One of the authors of this blog is Morgan Housel, author of The Psychology of Money and Same As Ever, partner at The Collaborative Fund.

The RSS's url is : http://feeds.feedburner.com/collabfund

Please copy to your reader or subscribe it with :

2024-05-01 03:03:00

Japan has 140 businesses that are at least 500 years old. A few claim to have been operating continuously for more than 1,000 years.

It’s astounding to think what these businesses have endured – dozens of wars, emperors, catastrophic earthquakes, tsunamis, depressions, on and on, endlessly. And yet they keep selling, generation after generation.

These ultra-durable businesses are called “shinise,” and studies of them show they tend to share a common characteristic: they hold tons of cash, and no debt. That’s part of how they endure centuries of constant calamities.

I love the quote from author Kent Nerburn that, “Debt defines your future, and when your future is defined, hope begins to die.”

Not only does hope begin to die, but the number of outcomes you can endure does, too.

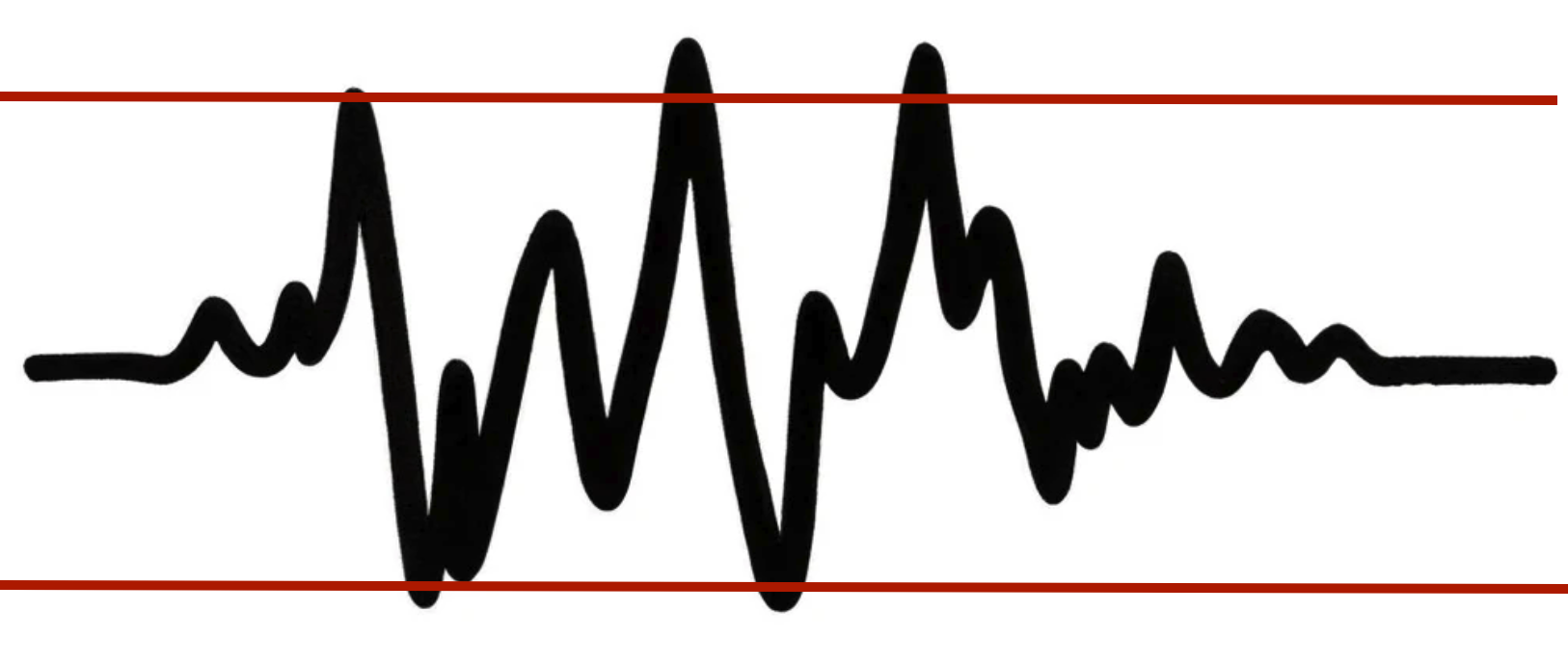

Let’s say this represents volatility over your life. Not just market volatility, but life world and life volatility: recessions, wars, divorces, illness, moves, floods, changes of heart, etc.

With no debt, the number of volatile events you can withstand throughout life might fall within a range that looks like this:

A few extreme events might do you in, but you’re pretty durable.

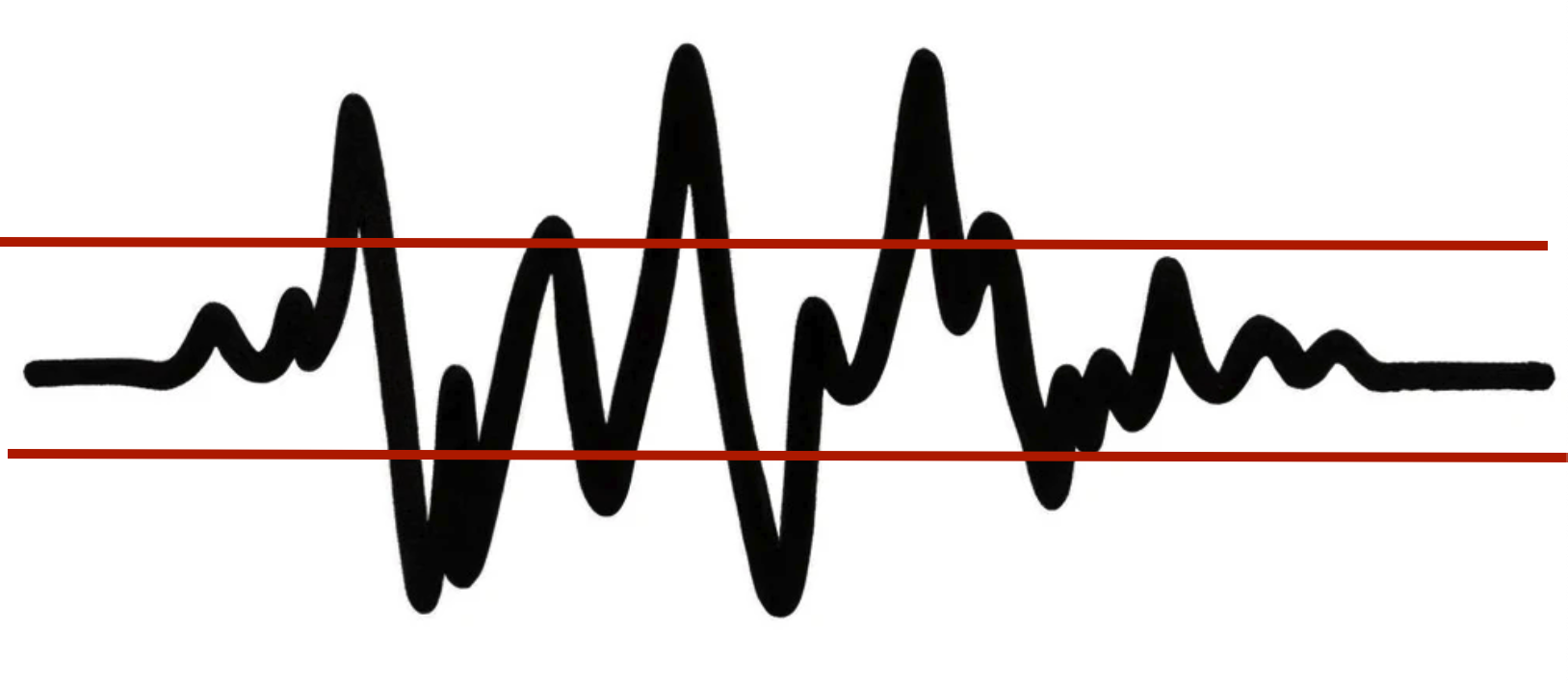

With more debt, the range of what you can endure shrinks:

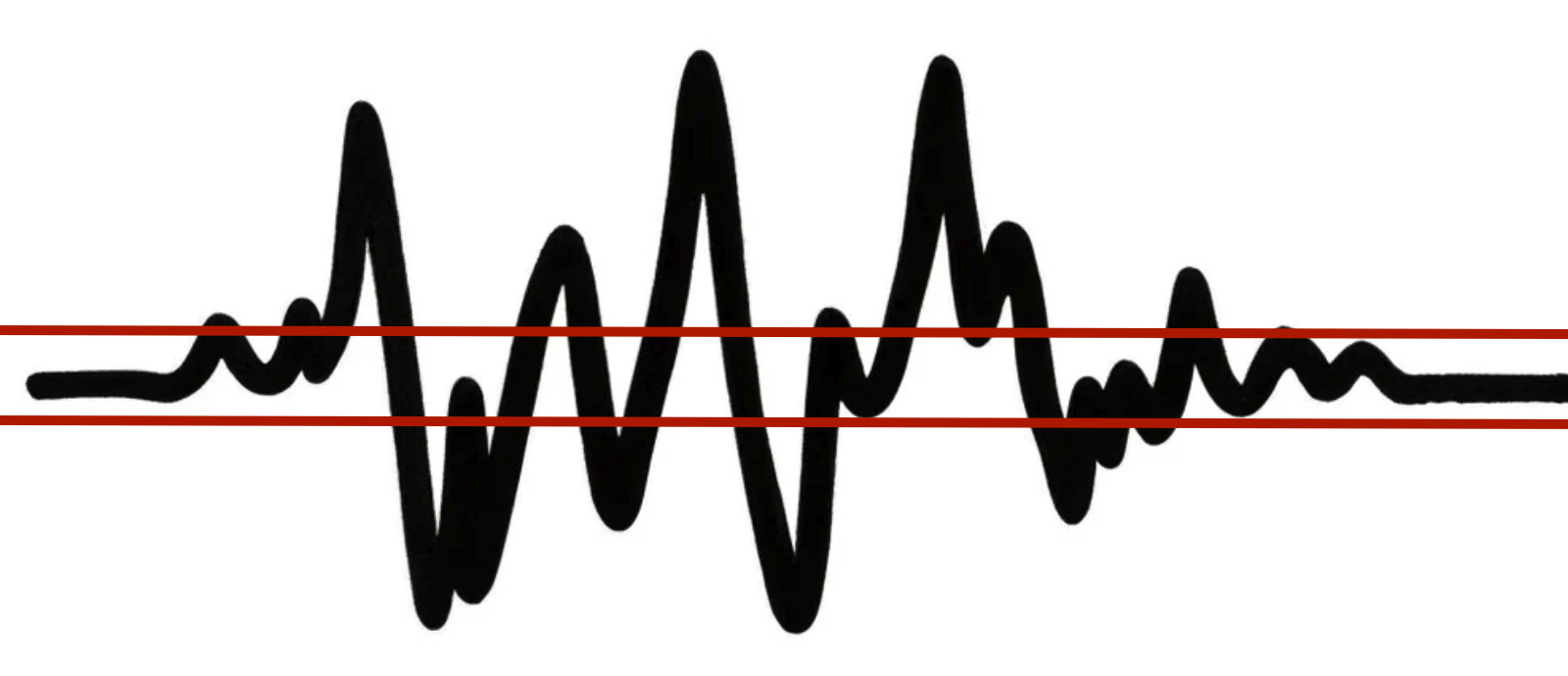

And with tons of debt, it tightens even more:

I think this is the most practical way to think about debt: As debt increases, you narrow the range of outcomes you can endure in life.

That’s so simple. But it’s different from how debt is typically viewed, which is a tool to pull forward demand and leverage assets, where the only downside is the cost of capital (the interest rate).

Two things are important when you view debt as a narrowing of endurable outcomes.

One is you start to ponder how common volatility is.

I hope to be around for another 50 years. What are the odds that during those 50 years I will experience one or more of the following: Wars, recessions, terrorist attacks, pandemics, bad political decisions, family emergencies, unforeseen health crises, career transitions, wayward children, and other mishaps?

One-hundred percent. The odds are 100%.

When you think of it like that, you take debt’s narrowing of survivable outcomes seriously.

The other is you think about the kinds of volatile events that could do you in.

Financial volatility is an obvious one – you find yourself unable to make your debt payments. But there’s also psychological volatility, where for whatever reason you can’t mentally endure your job any longer. There’s family volatility, which can be anything from divorce to caring for a relative. There’s child volatility, which could fill a book. Health volatility, political volatility, on and on. The world’s a wild place.

I’m not an anti-debt zealot. There’s a time and place, and used responsibly it’s a wonderful tool.

But once you view debt as narrowing what you can endure in a volatile world, you start to see it as a constraint on the asset that matters most: having options and flexibility.

2024-04-30 15:09:00

Thirty-seven thousand Americans died in car accidents in 1955, six times today’s rate adjusted for miles driven.

Ford began offering seat belts in every model that year. It was a $27 upgrade, equivalent to about $190 today. Research showed they reduced traffic fatalities by nearly 70%.

But only 2% of customers opted for the upgrade. Ninety-eight percent of buyers preferred to remain at the mercy of inertia.

Things eventually changed, but it took decades. Seatbelt usage was still under 15% in the early 1980s. It didn’t exceed 80% until the early 2000s – almost half a century after Ford offered them in all cars.

It’s easy to underestimate how social norms stall change, even when the change is an obvious improvement. One of the strongest forces in the world is the urge to keep doing things as you’ve always done them, because people don’t like to be told they’ve been doing things wrong. Change eventually comes, but agonizingly slower than you might assume.

Dunkirk was a miracle. More than 330,000 Allied soldiers, pinned down by Nazi attacks, were successfully evacuated from the beaches of France back to England, ferried by hundreds of small civilian boats.

London broke out in celebration when the mission was completed. Few were more relieved than Winston Churchill, who feared the imminent destruction of his army.

But Edmund Ironside, commander of British Home Forces, pointed out that if the Allies could quickly ferry a third of a million troops from France to England while avoiding aerial attack, the Germans probably could, too. Churchill had been holding onto hope that Germany couldn’t cross the Channel with an invasion force; such a daring mission seemed impossible. But then his own army proved it was quite possible. Dunkirk was both a success and a foreboding.

Your competitors can probably innovate and execute as well as you can. So every time you uncover a new talent you’re proud of, temper your thrill with the acceptance that other people who want to win as badly as you probably aren’t far behind.

Notorious BIG once casually mentioned that he began selling crack in fourth grade. He explained:

They [teachers] was always like, “Take the talent that you have and think of something that you can do in the future with it.”

And I was like, “Well, I like to draw.” So what could I do with drawing? What am I gonna be, an art dealer? I’m not gonna be that type. I was thinking maybe I can do big billboards and shit. Like commercial art.

And then after that I got introduced to crack. Haha, now I’m thinking, commercial art?! Haha. I’m out here for 20 minutes and I can make some real, real money, man.

Incentives drive everything, and most of us underestimate what we’d be willing to do if the incentives were right.

When Barack Obama discussed running for president in 2005, his friend George Haywood – an accomplished investor – gave him a warning: the housing market was about to collapse, and would take the economy down with it.

George told Obama how mortgage-backed securities worked, how they were being rated all wrong, how much risk was piling up, and how inevitable its collapse was. And it wasn’t just talk: George was short the mortgage market.

Home prices kept rising for two years. By 2007, when cracks began showing, Obama checked in with George. Surely his bet was now paying off?

Obama wrote in his memoir:

George told me that he had been forced to abandon his short position after taking heavy losses.

“I just don’t have enough cash to stay with the bet,” he said calmly enough, adding, “Apparently I’ve underestimated how willing people are to maintain a charade.”

Irrational trends rarely follow rational timelines. Unsustainable things can last longer than you think.

When the Black Death plague entered England in 1348, the Scots up north laughed at their good fortune. With the English crippled by disease, now was a perfect time for Scotland to stage an attack on its neighbor.

The Scots huddled together thousands of troops in preparation for battle. Which, of course, is the worst possible move during a pandemic.

“Before they could move, the savage mortality fell upon them too, scattering some in death and the rest in panic,” historian Barbara Tuchman writes in her book A Distant Mirror.

There’s a powerful urge to think risk is something that happens to other people. Other people get unlucky, other people make dumb decisions, other people get swayed by the seduction of greed and fear. But you? Me? No, never us. False confidence makes the eventual reality all the more shocking.

Some are more susceptible to risk than others, but no one is exempt from being humbled.

Dr. Dan Goodman once performed surgery on a middle-aged woman whose cataract had left her blind since childhood. The cataract was removed, leaving the woman with near-perfect vision. A miraculous success.

The patient returned for a checkup a few weeks later. The book Crashing Through writes:

Her reaction startled Goodman. She had been happy and content as a blind person. Now sighted, she became anxious and depressed. She told him that she had spent her adult life on welfare and had never worked, married, or ventured far from home – a small existence to which she had become comfortably accustomed. Now, however, government officials told her that she no longer qualified for disability, and they expected her to get a job. Society wanted her to function normally. It was, she told Goldman, too much to handle.

Every goal you dream about has a downside that’s easy to overlook.

Historian John Meecham writes:

When we condemn [the past] for slavery, or for Native American removal, or for denying women their full role in the life of the nation, we ought to pause and think: What injustices are we perpetuating even now that will one day face the harshest of verdicts by those who come after us?

This applies to so many things.

What is the modern version of cigarettes, which were doctor-recommended just a few generations ago? We didn’t know dinosaurs existed 200 years ago, which makes you wonder what else is out there that we’re oblivious to today. What company is the modern Enron, so obviously a fraud? What do most people – not a few wackos, but most of us – believe that will look something between hilarious and disgraceful 100 years from now?

A lot of history is just gawking at how wrong, how blind, people can be. Disastrously wrong, embarrassingly blind. Millions of people, all at the same time. When you then realize that today will be considered history in a few generations … oh dear. It’s unpleasant. But also fascinating.

Apollo 11 was the first time in history humans visited another celestial body.

You’d think that would be an overwhelming experience – literally the coolest thing any human had ever done. But as the spacecraft hovered over the moon, Michael Collins turned to Neil Armstrong and Buzz Aldrin and said:

It’s amazing how quickly you adapt. It doesn’t seem weird at all to me to look out there and see the moon going by, you know?

Three months later, after Al Bean walked on the moon during Apollo 12, he turned to astronaut Pete Conrad and said “It’s kind of like the song: Is that all there is?” Conrad was relieved, because he secretly felt the same, describing his moonwalk as spectacular but not momentous.

Most mental upside comes from the thrill of anticipation – actual experiences tend to fall flat, and your mind quickly moves on to anticipating the next event. That’s how dopamine works.

If walking on the moon left astronauts underwhelmed, what does it say about our own earthly goals and expectations?

John Nash is one of the smartest mathematicians to ever live, winning the Nobel Prize. He was also schizophrenic, and spent most of his life convinced that aliens were sending him coded messages.

In her book A Beautiful Mind, Silvia Nasar recounts a conversation between Nash and Harvard professor George Mackey:

“How could you, a mathematician, a man devoted to reason and logical proof, how could you believe that extraterrestrials are sending you messages? How could you believe that you are being recruited by aliens from outer space to save the world?” Mackey asked.

“Because,” Nash said slowly in his soft, reasonable southern drawl, “the ideas I had about supernatural beings came to me the same way that my mathematical ideas did. So I took them seriously.”

This is a good example of a theory I have about very talented people: No one should be shocked when people who think about the world in unique ways you like also think about the world in unique ways you don’t like. Unique minds have to be accepted as a full package.

More:

2024-04-25 03:50:00

After tapping in for par on the 18th hole at Augusta National with the sun setting behind its towering pines, Scottie Scheffler claimed his second Masters in three years. Shortly thereafter, the prior year’s winner, John Rahm, placed the green jacket on Scheffler’s broad shoulders cementing Scheffler at the top of the world rankings.

As I watched the ceremony unfold, it reminded me of something Scott Van Pelt said last spring when he was discussing Scheffler and Rahm’s respective paths to the top of the sport. Given they had nearly identical scoring averages (~68.6), I figured their paths were very similar. I could not have been more wrong.

See, Rahm’s ascent had come from “risk-seeking”, as evidenced by the fact that he was averaging more than 5.5 birdies per round through the middle of last season and was on pace to become the first PGA player to do so since 2000.

Meanwhile, Scheffler’s success had come from “risk-mitigation”, as evidenced by the fact that he had made a bogey (or worse) on fewer than 10% of the holes he had played. Coincidentally, he was also on pace to do something that hadn’t been done since 2000.

For all you golfers out there, this should be encouraging because it means success can come in multiple forms, so long as you are disciplined enough to stick to what best suits your game. The trouble is few are willing and/or able to do so. Instead, the vast majority of golfers endlessly pivot.

On one hole they choose to be aggressive and attempt to hit a par-5 in two, only to lay up on the next one. They hit aggressive putts on some holes, then lag putts on others. They play it safe and pitch out from behind trees on the front nine, only to attempt aggressive draws around them on the back.

Why?

Because they let their emotions get the best of them.

This is just the start.

Golfers often change their approaches mid-hole, mid-round, mid-season, and sometimes even mid-swing. It’s unquestionably manic. Yet, golfer behavior pales in comparison to investor behavior.

Investors are notoriously mercurial. We chase performance, buy high, sell low, and endlessly pursue fads. Bull markets convince us that we are brilliant, when in reality we are often just pawns in another wealth destroying bubble. Bear markets, on the other hand, force us to do things we had previously convinced ourselves we would never do (namely selling at the lows and stop committing to private investments).

This is precisely the reason why nearly every equity fund’s dollar-weighted returns are significantly worse than their time-weighted returns and why private equity vintage performance is inversely correlated to the amount of capital that funds have raised (i.e., the worst vintages typically come during buoyant fundraising periods). This behavior has been on full display over the past decade-and-a-half.

Like Jordan Spieth’s play in the years after he blew a five shot lead in the final round of the 2016 Masters, investors became incredibly risk averse in the wake of the 2007-2009 great financial crisis (“GFC”) after suffering extreme losses. This meant a strong aversion to riskier asset classes like high growth tech stocks and venture capital. However, as is almost always the case, this aversion waned over time as both started to post strong returns and animal spirits slowly returned.

As the GFC fell further into the rearview mirror, investors began shifting into risk-seeking mode and ratcheted up their exposures to these riskier assets, especially with bond yields so low. It started with modest commitments to venture and tech, but quickly ramped up towards the end of the decade.

For a while, things felt good. Check that, things felt great as the highest growth parts of the market posted eye-popping returns. After all, who doesn’t love the feeling of hitting shots like Phil Mickelson from behind the tree on the 13th at the 2010 Masters or Bubba Watson in a playoff at the 2012 Masters?

The trouble is, unlike Mickelson and Watson who rarely waver from their risk-on approaches, in 2022 when the NASDAQ fell 40% and venture seized up in the wake of Silicon Valley Bank’s failure amid higher rates, investors once again retreated into risk-mitigating mode by failing to add to beaten down tech companies and cutting back on new venture commitments.

When the markets then rallied unexpectedly in 2023 on the heels of the hype around AI and the prospect for lower rates, investors were once again left chasing.

So where does this leave us today?

Investors are once again in risk-seeking mode as evidenced by the fact that individual investors are the most bullish they’ve been since the fall of 2021, the NASDAQ is once again taking in record flows, and investor confidence is so high that buying protection against a 5% dip in the next year has fallen to what Bank of America strategist Ben Bowler called not too long ago the “cheapest you likely have ever seen”. All at a time when the markets look very expensive.

The question is, why do investors continually behave like this?

Simply because it is in our nature.

As Charlie Munger said,

“A lot of people with high IQs aren’t great investors because they have terrible temperaments. That is why having a certain kind of temperament is more important than brains. You need to keep raw irrational emotion under control. You need patience and discipline and an ability to take losses and adversity without going crazy. You need an ability to not be driven crazy by extreme success.”

This quote was top of mind when someone recently asked me whether I thought we should materially dial back risk for an institution I serve on the investment committee for. Earlier in my career, I likely would have responded that we absolutely should dial risk back given the current state of valuations, cheap cost to protect via options, extreme confidence, and looser credit conditions. However, the longer I do this, the more I realize the answer is significantly more nuanced.

The fact is I have no idea where markets are headed or whether there is a greater chance markets will crash or compound at reasonable rates of return over the next few years. No one does.

That said, how did I respond?

I simply said that I thought we should stick to our process.

Now, since this particular institution is conservative in nature, has significant outstanding obligations over the next few years, and no meaningful pending inflows of new capital, this meant that yes, we likely should be more defensive and dial back our risk (the same could be said for a 70-year old retiree with no incoming cash flows or someone looking to retire in the next few years).

However, if this institution had a more “risk on” nature, few (if any) future fixed obligations, and a reliable stream of capital inflows, I would likely have said that it did not make as much sense to significantly dial back risk — namely to skip venture capital commitments, rush out of equities into bonds, etc. (the same could be said for a person early or in the prime of their careers with decades left to work and generate income). The reason is simply because doing so would mean straying from its process, timing the market, and maybe most importantly, forcing a future decision on when to switch back into risk-seeking mode…something few can do effectively.

So, what’s the bottom line?

Investing is hard, but it doesn’t need to be as hard as people make it. As John Rahm and Scottie Scheffler illustrate, success can come in very different forms, so long as you consistently adhere to your process.

Risk-seeking and risk-mitigating can both be successful strategies, so long as you are disciplined enough to stick to them. So today, while the market feels a bit frothy, inflation remains stubbornly high, and the risk to the downside feels greater than the potential to the upside, history has shown that trying to materially adjust your approach to fit the current environment as opposed to your unique circumstances doesn’t typically work out well. Only the very elite (or lucky) investors have shown an ability to toggle between risk-seeking and risk-mitigating.

Now before you go thinking you might be elite, remember when I said earlier that both Rahm’s 5.5 birdies per round and Scheffler’s <10% bogey threshold were coincidentally last accomplished in 2000? Care to guess which golfers accomplished those thresholds close to two-and-a-half decades ago?

Well, what if I told you it wasn’t multiple golfers?

What if I told you it was just one?

Tiger Woods.

So, unless you are the investing equivalent of the greatest golfer of all-time, it probably makes sense to stick to one or the other.

2024-04-08 11:13:00

Luck plays such a big role in the world. But it’s hard to talk about. If I say you got lucky, I look jealous. If I tell myself that I got lucky, I feel diminished.

Maybe a better way to frame luck is by asking: what isn’t repeatable?

Lucky implies random events you could not see coming. What isn’t repeatable is different. Did Jeff Bezos get lucky creating Amazon? Not in the same way a lottery winner is lucky, of course. He was visionary and ambitious and savvy to a degree you only see a few times per century.

But could he, starting today, without any money or name recognition, create a new multi-trillion dollar business from scratch?

Maybe, but probably not. There are so many things that helped Amazon become what it is that can’t be replicated – growth of the internet, market conditions, old competitors, politics, regulations, etc. Bezos is enormously skilled in a way that is not luck. But a lot of what he did was not repeatable. Those points are not contradictory.

It’s so important to know the difference between the two when attempting to learn from someone. You want to try to emulate skills that are repeatable. Attempting to copy the parts of someone’s success that aren’t repeatable is equivalent to a 56-year-old dressing like a teenager and expecting to be cool.

There’s a law in evolution called Dollo’s Law of Irreversibility that says once a species loses a trait, it will never gain that trait back because the path that gave it the trait in the first place was so complicated that it can’t be replicated. Say an animal has horns, and then it evolves to lose its horns. The odds that it will ever evolve to regain its horns are nil, because the path that originally gave it horns was so complex – millions of years of selection under specific environmental and competitive conditions that won’t repeat in the future. You can’t call evolutionary traits luck – they came about because of very specific forces. You just can’t ever rely on those forces repeating themselves exactly as they did in the past.

A lot of things work like that.

In business and investing, you want to learn the big lessons about why things behave the way they do without assuming the past is a direct guide to the future, because it’s not – most of the details are not repeatable. History is the study of change, ironically used as a map of the future.

Jason Zweig of the Wall Street Journal once talked about what happens when you try to learn a very specific, non-repeatable lesson when a broader, very repeatable lesson is what you needed to pay attention to:

[After the dot-com crash], the lesson people learned from that was not, “I should never speculate on overvalued financial assets.” The lesson they learned was, “I should never speculate on internet stocks.” And so the same people who lost 90% or more of their money day-trading internet stocks ended up flipping homes in the mid 2000s, and getting wiped out doing that. It’s dangerous to learn narrow lessons.

The great thing when you ask, “is this repeatable?” is that you start to focus on things that you and I – ordinary lay people – have a chance of repeating ourselves.

You can learn a lot from Warren Buffett’s patience. But you can’t replicate the market environment he had in the 1950s, so be careful copying the specific strategies he used back then.

You can learn so much from John D. Rockefeller about the importance of controlling distribution. But you cannot replicate the 20th century legal system that allowed him to destroy competitors, so don’t get carried away there.

Elon Musk can teach you a lot about risk-taking and branding, but much less about competing in the auto business.

Jeff Bezos can teach you so much about management and long-term thinking, but much less about e-commerce and cloud computing.

The way to get luckier is to find what’s repeatable.

2024-03-28 23:42:00

We are inundated these days with headlines about how our college system is broken and how despondent graduates are due to things like outsized student loan debt.

Are these claims merited?

Undoubtedly.

Should more kids be considering the pros vs. cons on paying $100-200 thousand dollars to attend college?

You bet.

But is that the whole story?

Of course not.

The fact is, like most things in life, there is another side of this story that isn’t getting nearly as much attention.

America currently produces nearly twice as many college graduates as it did just two decades ago (from less than 1.3 million in 2000 to more than 2.1 million in 2022). Yet, over this same period, America’s top colleges, as judged by the U.S. News & World Report rankings, have not increased their enrollment numbers in any measurable way. Look no further than Harvard, which has not increased its freshman class in more than three decades (it was roughly 1,600 in 1990 and is roughly 1,650 for the class of 2023).

So why does this matter?

It matters because it has created a supply/demand imbalance between the number of qualified candidates applying for college and the number of available spots at the top schools.

So, who is impacted by this imbalance?

In short, everyone.

However, a disproportionate amount of the impact falls on the students, the companies trying to hire them, and cities across the country where graduates flock to.

Said another way, this new imbalance has caused a “spillover effect” whereby highly qualified students who used to largely matriculate to universities in the Northeast or California are now attending colleges across the entire country. Look no further than the fact that the average SAT score at The University of Florida is now 1420 for in-state students and 1450 for those out-of-state. When I was applying for college two-and-a-half decades ago, those scores would have gotten you into nearly any school of your choice. Now they are the average score for a state university with over 40,000 students. It is the same story at countless other universities across the country.

This means that talented young people are more spread out than ever. It also means that thanks to programs like the Hope Scholarship in Georgia and Bright Futures Scholarship in Florida, more accomplished students are staying in-state, attending large schools, and building out their networks. As a result, the ecosystems around these universities and in the surrounding cities are larger than ever, which is creating more dynamic talent pools, better business formation, and greater entrepreneurship in many communities across the country.

Yet, despite these developments, my impression is that many companies and investment funds have yet to tap into this development in a meaningful way.

But, what if they did?

I recently met someone who has and the results speak for themselves.

A couple months ago, I attended an annual meeting for a national defense-focused venture capital firm at Cavallo Point, which is a hotel that lies practically in the shadow of the Golden Gate Bridge.

On the second night, I sat next to someone at dinner who I will call “Rick”. Considering the nature of this meeting, Rick was straight out of central casting given his strong resemblance to Slider from the original Top Gun.

Rick and I had several conversations throughout the night ranging from being disillusioned Washington Commanders’ fans to growing up in military families. Yet, the part that stood out the most was something he said about his last few years running a division at one of the top banks on Wall Street.

Before I get to this though, it is important to provide a bit more on Rick’s background, none of which I found out until I Googled him when I got back to my hotel room later that night.

See, Rick had been an All-Ivy and All-American college athlete, while simultaneously doing the Reserve Officer Training Corp (“ROTC”) program. After graduation, he served five years as a marine, went to Stanford Business School, joined one of the top banks on Wall Street, did multiple tours in Iraq and Afghanistan after 9/11, served in a presidential administration, wrote multiple books on military affairs, and completed several Ironmans. Yet he barely mentioned any of this during our conversation. Humility is a vastly underappreciated quality these days, but I digress.

Now back to his last few years on the trading desk.

Rick told me that after returning from his second tour of duty, he rejoined his desk and within a short period of time was asked to lead it. In this role, part of his responsibility was to recruit and make new hires. The trouble was that as the years passed, he was finding it increasingly difficult to recruit and retain effective young people from the desk’s seven “target schools” (you can probably guess which ones they are).

Hearing this, I was a little dumbfounded.

How could this guy not find effective people to join him on one of Wall Street’s best desks? Heck, I would have run through a brick wall to work for this guy after sitting next to him for an hour.

This said, with a confused look on my face, I asked him flatly,

“How is that possible? How did you not have the ‘pick of the litter’?”

He replied,“That’s the thing. We actually did. The problem is it wasn’t a matter of talent or intellect. We were getting the top kids from some of the top schools in the country.”

He explained that the problem ran much deeper. While these kids had plenty of intellect, he found that they were lacking something else. Something much more important.

Rick described how at some point during the past few years, the balance started to shift from these new recruits feeling as if they owed the firm something to a belief that it owed them. The job was simply a short-term pit stop on their way to the next part of their careers. As a result, their effort, enthusiasm, and productivity had deteriorated materially versus prior “classes”. Remote work only accelerated and accentuated this trend.

As I digested this new reality, I asked him how he responded.

His answer was predictably simple — “I looked elsewhere.”

While he continued to recruit from the seven target schools, Rick added seven “non-targets,” only instead of simply moving down the list in the US News & World Report rankings, he chose a different set of criteria.

He targeted large universities across the country with students from a wide range of backgrounds. Within these schools, he looked for those who had put themselves in leadership positions, be it in ROTC, sports, a fraternity or sorority, student government, or the arts, among other things, so long as they had taken ownership of something. Preferably, he wanted to see examples of resilience and persistence in these pursuits. In short, he was looking for kids who had embraced and indulged in everything the university had to offer, all while excelling academically.

After selecting and visiting these schools, his desk hired five analysts from the “non-target” schools and another six from the traditional “target schools”. Then, after these eleven analysts completed their first year on the desk, they were ranked.

Care to take a guess as to how the rankings shook out?

You probably see where this is headed.

The analysts from the “non-target” schools ranked something like #1, #2, #4, #5, and #7, while the analysts from the traditional “target” schools claimed the #3, #6, and #’s 8-11 spots.

The results were so stark that the firm’s CEO approached Rick to see what drove them. Rick’s response was direct and clear — The analysts from “non-target” schools simply wanted it more. They were humble and wanted to learn. They were willing to go above and beyond what had been asked of them. Much like how I felt just talking to this guy, these kids wanted to run through a brick wall for him.

After talking to Rick, the CEO apparently revamped the firm’s recruiting process. Today, each area of the firm is allowed to incorporate a “non-target” school list in addition to their target list. Apparently, the results speak for themselves.

My takeaway?

This country has challenges and the higher education system is near the top of the list. However, one thing that is far from challenged is its vast depth of talented, driven, hopeful, and resourceful young people. The key for businesses looking to hire young talent or investors trying to find the next great company is to seek out and identify these young people and give them the opportunity to shine.

So, what does this look like?

It starts with doing what Rick did — acknowledging that continuing to fish in a few select ponds that haven’t grown in more than three decades probably isn’t the optimal way to source talent anymore. Instead, it means stretching your hiring lens, looking in places you haven’t before, and taking chances on less conventional candidates in order to find diamonds in the rough.

Now, don’t get me wrong. This does not mean disregarding traditional recruiting hotbeds and target schools. That would be like telling an NFL general manager to no longer draft players from the SEC because the talent in other conferences has improved. Instead, it simply means that expanding your hiring horizon should be additive to performance.

At the end of the day, for all the young people out there looking to land their dream job, there is one thing you can do that is fully within your control that transcends where you went to college, what you majored in, what your background looks like, or where you are from. UFC president Dana White said it best,

“Just be a savage. These days, if you are even remotely a savage and you get out there and you grind hard and you want it badly enough, you can run by anyone. It is all out there for the taking, especially in this era of remote work. There has never been more opportunity out there than there is today.”

And for the companies and investors looking to excel and outperform?

Start by finding these savages.

2024-03-25 07:34:00

A few smart things I’ve read recently:

“People in their 30s know where the world is going because they’re going to do it. I’m in my 80s so I have no idea.” - Daniel Kahneman

“Every group of people who think for a living is going to be sad. Ignorance is bliss. So what’s the opposite?” – Chris Rock

“I would say the most dangerous thing in the world with a 12-year-old is to try to be his friend. But the worst thing with a 40-year-old is to try to be their parent.” - Chris Davis

“Schopenhauer’s ideal is to be wealthy enough to have expansive free time and the intellectual capabilities to fill it with contemplation and activity in the service of mankind.” – Derren Brown

“If you ask yourself why you are in business and can find no answer other than ‘I want to make money,’ you will save money by getting out of business and going to work for someone.” – Harvey Firestone

“When asked what was the best asset a man could have, Albert Lasker — the most astute of all advertising men — replied, ‘Humility in the presence of a good idea.’ It is horribly difficult to recognize a good idea.” – David Ogilvy

“I became so avid a collector of instances of bad judgment that I paid no attention to boundaries between professional territories … why should I search for some tiny, unimportant, hard-to-find new stupidity in my own field when some large, important, easy-to-find stupidity was just over the fence in the other fellow’s professional territory? – Munger

“The more I am around horse racing the more I think that the most underrated thing is the horse and that it is us trainers and jockeys and owners who are overrated.” – Leroy Jolley

“We are built with an almost infinite capacity to believe things because the beliefs are advantageous for us to hold, rather than because they are even remotely related to the truth.” – Dee Hock

“When momentum is on your side, people focus on your strengths and forgive your weaknesses. When the momentum stops, they scrutinize the whole thing.” – Packy McCormick

“Join no creed, but respect all for the truth that is in them.” – Robert Henri

“Apple was Steve Jobs with 10,000 lives.” – David Senra

“I wanna see your best work. I’m not interested in your new work.” – Jerry Seinfeld

Jonas Salk, inventor of the polio vaccine, said the main motivation of his life was, “To be a good ancestor.”

“A great way to understand yourself is to seriously reflect on everything you find irritating in others.” – Kevin Kelly

“The world is split between those who don’t know how to start making money and those who don’t know when to stop.” - Taleb

“It doesn’t take much to convince us that we are smart and healthy, but it takes a lot of facts to convince us of the opposite.” – Dan Gilbert

“Happiness is that feeling you get right before you need more happiness.” – Don Draper

“Notice that, while lots of people are happy to tell you about Golden Ages, nobody ever seems to think one is happening right now. Maybe that’s because the only place a Golden Age can ever happen is in our memory.” – Adam Mastroianni

“I believe pretty strongly that one’s overarching aim in life and work is to always be making one’s self obsolete.” – Tim Hanson

“It is a curious feature of our existence that we come from a planet that is very good at promoting life but even better at extinguishing it.” – Bill Bryson

“Fast growth is counterintuitively more perilous than declining revenue and can quickly destroy a company.” – Brent Beshore

“If passionate love is a drug—literally a drug—it has to wear off eventually.” – Jonathan Haidt (I think this applies to everything from relationships to businesses. Curiosity is more sustainable than passion).

“Better to get your dopamine from improving your ideas than having them validated.” – Nat Friedman

“People with very high expectations have very low resilience.” – Jensen Huang

It’s good to be optimistic in the general and skeptical in the specific. It’s very dangerous to be pessimistic in the general and optimistic in the specific. – Naval (paraphrasing)

“The greatest trick the devil ever played was making you believe that the pessimists are the good guys.” – Packy McCormick

2024-03-04 08:32:00

Most people will die after three days without water. But drinking too much can be equally dangerous – water intoxication is deadly, and during rigorous training about a dozen soldiers per year are hospitalized for drinking too much water.

Mae West said, “Too much of a good thing can be wonderful.” That might be true for some things – health, happiness, golden retrievers, maybe.

But in so many cases the thing that helps you can be taken to a dangerous level. And since it’s a “good thing,” not an obvious threat, its danger creeps into your life unnoticed.

Take intelligence. I’m talking about book intelligence, the kind that shows up in SAT scores and GPAs.

How could someone possibly be too intelligent? How do you get to a point where you realize you could have been more successful if you had been a little dumber?

A few big ways:

1. Very smart people can fool themselves with elaborate stories about why something happened.

Comedian Robin Williams was a terrible student. During a macroeconomic class at College of Marin, Williams’ final paper contained a single sentence to his professor: “I really don’t know, sir.”

He failed the test, but it’s the right answer to most economic problems.

There is so much that we not only don’t know, but can’t know, about why complex systems like the stock market and economy behave the way they do, because human emotions and shifting social preferences can’t be distilled down to a formula. Humility is a superpower that prevents overconfidence.

But being very smart makes it harder to harness that humility. You want to put your big brain to work, and your mental horsepower allows you to create complex stories and elaborate models of cause and effect. Worse, if you believe that complexity equals intelligence and intelligence equals accuracy, you favor the explanation that strains your brain the most.

If asked, “Why did the stock market fall 0.23% last week?” an average person will shrug their shoulders and walk away. A very smart person will show you their yield-curve model and valuation analysis and tell you whether the performance will continue. Who do you think is more likely to be stricken by overconfidence?

I’ve come to believe that part of the reason professional money managers produce such lousy returns is because the industry attracts such intelligent people. They’re too smart for their own good. There’s a fine line between intellectual rigor and believing your own bullshit, and smart people are at more risk than ordinary folks.

2. Being very smart makes it harder to listen to people who are less credentialed than you, even when they might have the right answer.

Being smart is almost a tribe in itself, and like all tribal affiliations it becomes hard to view outsiders as equals.

The amount of time, money, and stress it takes to get a degree, or become senior vice president, or win an award, can lead you to believe that others who lack those accomplishments cannot offer valuable insight. Doing so makes you question why you put so much effort into your credentials to begin with.

It’s amazing what happens when you become open to the best ideas, rather than the most credentialed voices.

One of the funniest scenes from Seinfeld is the episode Jerry at the Dentist. Before putting the nitrous oxide mask on his patient, the dentist inhales the gas himself and declares, “Yep, it’s good.”

The whole scene was an accident. Bryan Cranston, who plays the dentist, later revealed where the joke came from:

As we’re rehearsing I hear someone say, “Hey, you know what would be funny?” And I look around the set and I see a [stagehand] adjusting a light. And he goes, “It’d be funny if before you gave it to Jerry, you took a hit yourself.”

And I went, “Oh my god, that is funny.”

Cranston’s takeaway is great:

I think a very smart CEO of any company, big or small, has a policy where they listen to every suggestion and idea — best idea wins. That’s how it should be. Best idea wins. And you never know where it’s gonna come from.

You can see how this could become dangerous in something like medicine or nuclear physics, where the cost of ignorance is extreme – a brain surgeon shouldn’t ask for tips offered by the janitor.

But in many industries it’s not appreciated enough. I often wonder how many tens of billions of dollars have been paid to management consultants to solve problems that low-wage line workers had solutions for, only because a guy in a suit has a hard time taking a guy with dirty fingernails seriously.

3. Having an intellectual reputation to maintain can make it difficult to change your mind when you need to.

I saw an amazing stat yesterday. LeBron James has now scored 40,000 points in the NBA, and each 10,000-point increment was earned in almost the exact same number of games:

10K in 368 games

10K to 20K in 358 games

20K to 30K in 381 games

30K to 40K in 368 games

Consistency. It’s astounding when you see it, the hallmark of a true talent.

But there’s a danger in some fields when a smart person becomes known for their consistency in doing something, and then the world evolves away from that thing, but the person is desperate to hold onto the perceived consistency of their talent.

If a smart person becomes known as, “The guy who can forecast the oil market.” Or, “The woman who can predict the next election,” you run the risk that you were only an expert on a version of the world that no longer exists.

If the world evolves, you should probably either find a new area to apply your intelligence, or alter your confidence, or at least change the way you work and the product you deliver.

But if the rest of the world craves your consistency, you can’t.

They want you to keep doing the same thing over and over.

And you want that too, because you want to guard your intellectual reputation. You marketed yourself as an expert in a specific thing, so it’s hard to evolve into something else.

If you become famous for your smart ideas, but those ideas turn out to be either wrong or outdated, it’s extremely difficult to move on. The result is a lot of very smart people clinging to very bad ideas.

A hedge fund manager who had a moment of brilliance and made a fortune in the 1990s might struggle to adapt, because their ego and their investors expect them to repeat whatever worked last time. A garbageman doesn’t face that risk. They are much more attuned to the current reality, without the intellectual baggage of past accomplishments.

The biggest risk to an evolving system is that you become bogged down by experts from a world that no longer exists. The more evolution you have, the more you should expect that expertise has a shelf life. And those most susceptible to that risk are the people you’d least suspect: The smartest and most intelligent, who at one point flashed their brilliance but struggled to admit that it can’t be repeated.

2024-02-01 04:50:00

There are two ways to use money. One is as a tool to live a better life. The other is as a yardstick of status to measure yourself against others. Many people aspire for the former but get caught up chasing the latter.

Money is a tool you can use. But if you’re not careful, it will use you. Sometimes the stuff you spend money on has so much influence over your autonomy and sanity that it’s not clear whether you own things or the things own you.

Everyone can spend money in a way that will make them happier, but there is no universal formula on how to do it. The nice stuff that makes me happy might seem crazy to you, and vice versa. Like many things in finance, debates over what kind of lifestyle you should live are often just people with different personalities talking over each other.

How you spend money can be a reflection of what you’ve experienced in life. To someone who grew up snubbed by poverty, owning a fancy car might be the ultimate symbol of what you’ve overcome. To an old-money family, it might be the ultimate symbol of ego and insecurity. People don’t just spend money on things they find fun or useful. Their decisions often reflect the psychological wounds of their life experiences.

Spending money can buy happiness, but it’s often an indirect path. The big, nice house might make you happier, but mostly because it makes it easier to spend time with friends and family, and the friends and family are actually what are making you happy.

Unspent money buys something intangible but valuable: freedom, independence, autonomy, and control over your time. Every dollar of savings buys a claim check on the future.

At the same time, some wealthy people struggle to spend money on things that would make them happy because “I’m a saver” becomes such an ingrained part of their identity. What you intended to be a strategy to achieve a better life turns into an ideology you are beholden to.

There are cases when people’s desire to show off fancy stuff is because it’s their only way to gain respect and admiration. Everyone wants respect and admiration, a feeling that they matter and are needed. Some people who feel they aren’t getting respect for their intelligence, humor, wisdom, or ability to love resort to trying to get it by impressing you with their car, house, or clothes.

Nothing is as desired as much as the thing you want but can’t have. Material goods that play hard to get mess with our heads the same way people do. When something you like is just out of reach – you can almost afford it, but not quite yet – it takes on a mystique and exaggerates the dreams you have about how much that thing will make you happy and solve your problems.

Aspirations trickle down. Kevin Kelly once made the point that if you want to know what lower-income groups will aspire to spend their money on in the future, look at what higher-income groups do today. European vacations were once the exclusive playground of the rich. Then they trickled down. Same with college, investing in the stock market, two-car households, lawns, walk-in closets, and six-burner stoves – what was once a luxury of the rich became standards of the masses.

There is no such thing as an objective level of wealth. Everything is relative to someone else. People look around and say, “What’s that person driving, where are they living, what kind of clothes are they wearing?” Aspirations are calibrated accordingly.

There’s a difference between nice stuff and fancy stuff. One provides tangible utility, the other offers social utility. Someone once noted that a high-end Toyota is a better car than an entry-level BMW, because the nice Toyota is filled with things that make driving more pleasant, while the entry-level BMW is mostly just status and bragging rights. Using money to buy nice stuff is great. Fancy stuff is a different, more complicated, animal.

The more money you have, the harder it becomes to know how to spend it in a way that will make you happy. And that confusion sets in at fairly low levels of income. Luke Burgis writes: “After meeting our basic needs as creatures, we enter into the human universe of desire. And knowing what to want is much harder than knowing what to need.”